A practical guide on how to protect your 401k during a market crash using diversification, rebalancing, and behavior safeguards.

Sectors & Industries

February 11, 2026

Table of Contents

A 401(k) is built for decades, but the damage usually happens in months—when a sharp drawdown meets bad behavior. Protecting your 401(k) during a crash is less about “predicting the next recession” and more about building a system that (1) reduces forced selling, (2) keeps you diversified and rebalanced, and (3) blocks panic decisions when volatility spikes.

Below is a practical, U.S.-only playbook that combines institutional portfolio design with real-world 401(k) constraints (limited menus, stable value rules, target-date fund glide paths, and plan-level restrictions).

Most long-term investors don’t fail because markets go down. They fail because they sell when markets go down and/or stop contributions when their future returns are cheapest.

A crash becomes permanently damaging when it triggers:

Your defense is to make the “right move” the default move.

In a 401(k), you don’t get fancy. You get disciplined.

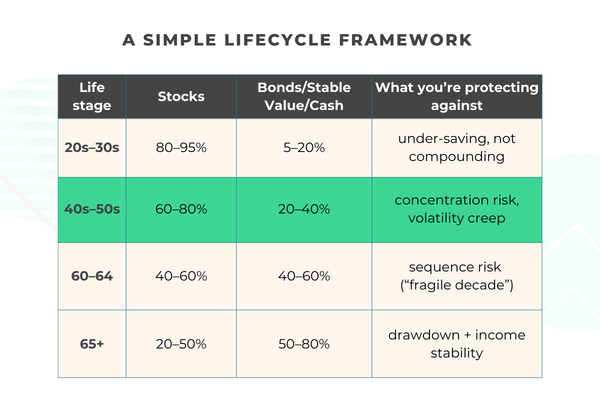

Asset allocation is your primary crash protection because it controls how much your portfolio can fall—and how easily you can rebalance into recovery.

Key rule: If you’re within ~10 years of retirement, you should be thinking in drawdown terms, not “average return” terms.

Diversification isn’t “owning lots of funds.” It’s owning assets that behave differently under stress.

In 401(k) terms:

If your plan offers company stock, be careful. A corporate downturn can hit:

If you do nothing else, at least cap employer stock exposure to a level that won’t wreck your retirement if your employer has a bad decade.

If your plan offers a stable value fund, it can be one of the best “shock absorbers” available inside a 401(k)—often yielding more than money markets without the price volatility of bond funds.

But stable value funds come with fine print:

When stable value makes sense:

Target-date funds (TDFs) are often mocked as “set and forget,” but they have a real crash advantage: they rebalance automatically.

That matters because during a drawdown:

That’s institutional behavior most individuals fail to execute manually.

If you’re using a TDF, the real decision is not “TDF or not,” it’s:

Crashes create “decision density”—too many choices, too much emotion.

So you want guardrails:

A simple crash plan:

Some 401(k)s offer an SDBA (brokerage window). It can help you add diversifiers your core menu doesn’t have, but it can also increase mistakes.

If you go this route, keep it tight:

This is where AI monitoring can matter.

A wealth manager like Michael Flatley typically doesn’t “guess” crashes—he runs managed portfolios with risk controls, then uses AI-driven monitoring to stay ahead of catalyst-driven volatility (earnings shocks, guidance cuts, layoffs, regulatory actions, liquidity events). Tools like LevelFields fit that workflow by flagging market-moving events in real time—useful for risk reviews and position triage when you’re managing a household balance sheet that includes rollovers, taxable accounts, and concentrated exposures. In a 401(k), you can’t always act with precision, but you can use the same intelligence layer to avoid being the last person to understand why something broke.

If you’re within ~10 years of retirement—or already drawing—your goal is to avoid selling stocks at depressed prices.

The cleanest method is a cash/bond runway:

This turns a crash into a time problem, not a forced-selling problem.

Two things to keep on your radar:

The IRS announced the 2026 elective deferral limit is $24,000 for 401(k)/403(b)/457 plans, and the age 50+ catch-up remains $7,500.

SECURE 2.0 added rules requiring certain higher-wage earners to make catch-up contributions as Roth, but the IRS provided an administrative transition period through taxable years beginning after December 31, 2025.

(Translation: plan rules and payroll systems are still catching up, so you should verify what your specific plan is implementing and when.)

A resilient 401(k) isn’t one fund. It’s a structure:

You cannot lose your 401(k) outright unless you sell at the bottom or your investments go to zero (which diversified funds do not). What you can lose is account value temporarily. Losses become permanent only if you panic-sell during a crash or withdraw too much too early.

Key point: crashes hurt balances; behavior determines damage.

There is no single “pre-crash” fund that works for everyone. The correct move depends on time to retirement:

Trying to “guess” the crash usually causes more harm than the crash itself.

Yes—but protection is structural, not predictive.

Effective protection includes:

Recessions are survivable. Poor reactions are not.

There is no completely risk-free option that also preserves purchasing power.

Common “safe” options inside 401(k)s:

Safety always trades off against long-term growth.

It depends on spending, not the number.

As a rough benchmark:

It’s possible—but only with modest spending and careful planning.

During a crash, the worst move is rushing entirely to cash after prices fall.

Better priorities:

Professionals manage this by rules, not emotions. Wealth managers like Michael Flatley don’t try to predict crashes—they structure portfolios to withstand them and use tools such as LevelFields to monitor when real risk events occur, so decisions are informed rather than reactive.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE