.png)

L2 Weekly Stock Market News Analysis

December 14th, 2025

TLDR:

Markets ended the week steadier than they started, but the mood remained cautious. Stocks bounced as short-term funding fears eased and investors digested a quieter flow of headlines, helping stabilize sentiment after a volatile stretch driven by trade tensions and policy uncertainty.

Hopes for lower interest rates continued to support equities. Recent data showing slower hiring and easing inflation kept expectations alive for a Fed rate cut, even as policymakers signaled they may move carefully rather than rush into multiple cuts. That mixed message helped stocks stabilize, but also left investors uncertain about how much real relief lower rates will provide.

At the same time, cracks began to show in one of the economy’s strongest pillars: AI and data-center spending. Oracle disclosed delays in large data-center projects tied to AI workloads, pushing some timelines out by a year. Demand hasn’t disappeared, but the delay raised questions about how quickly this investment will feed into growth — especially since data centers have been doing much of the heavy lifting for the U.S. economy this year.

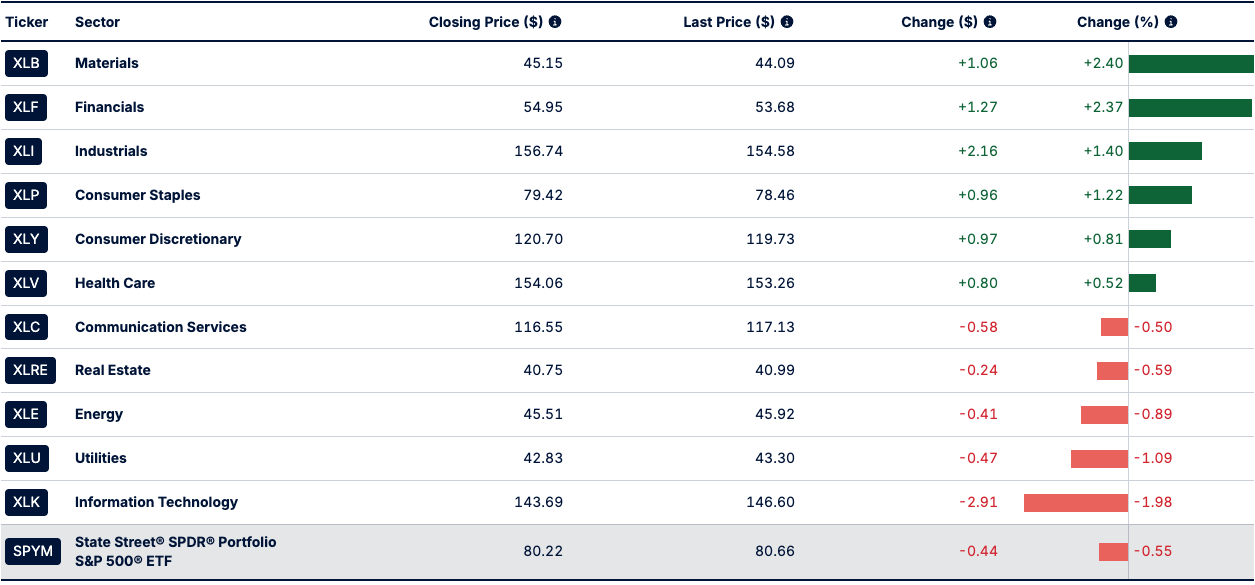

That tension showed up clearly in sector performance. More cyclical and economically sensitive areas led the market, with Materials (XLB) up 2.40%, Financials (XLF) up 2.37%, and Industrials (XLI) up 1.40%, reflecting renewed interest in infrastructure, balance-sheet strength, and nominal growth. Consumer Staples (XLP) and Consumer Discretionary (XLY) also finished higher, pointing to selective risk-taking rather than a full defensive shift.

Meanwhile, Technology (XLK) was the weakest major sector, falling 1.98%, as rising yields and growing scrutiny around AI spending timelines weighed on sentiment. Utilities (XLU), Energy (XLE), and Real Estate (XLRE) also lagged, while Communication Services (XLC) gave back recent gains alongside broader tech weakness.

Markets Got What They Wanted — The Final Cut of 2025

Markets opened the week focused on one outcome — and they got it. The Federal Reserve delivered a third consecutive 25 bp cut, lowering the policy range to 3.5%–3.75%, a move widely viewed as the final rate cut of 2025 and very likely the last cut of Jerome Powell’s term as Fed Chair.

Powell described the move not as the start of a new easing cycle, but as the completion of a normalization process — meaning the Fed believes it has now undone the most restrictive part of its post-inflation tightening without tipping the economy into recession. After three cuts since September, policymakers see rates as having moved from clearly restrictive toward neutral, reducing pressure on hiring and credit-sensitive sectors while still remaining high enough to keep inflation trending lower.

The Fed paired that message with modest upgrades to its 2026 growth outlook, small downward revisions to inflation forecasts, and repeated emphasis that much of today’s inflation pressure reflects tariff-related cost pass-through, which officials expect to fade over time. Just as importantly, Powell made clear that normalization does not imply continued easing. The policy statement reverted to more cautious language around “the extent and timing” of future adjustments, signaling a much higher bar for additional cuts.

In short: the Fed believes it has done enough to stabilize the economy — and is now prepared to wait.

A Split Fed — And Why That Matters

The rate cut was approved on a 9–3 vote, highlighting unusually sharp disagreement within the Fed over the path of policy. Two regional Fed presidents preferred no cut at all, while one governor argued for a larger 50 bp reduction. That split matters because it shows the Fed is not aligned on what comes next — some officials already think rates are low enough, while others worry the economy may need more support.

Immediately after the decision, Treasury yields fell sharply because investors focused on the cut itself and assumed policy would keep moving easier. When markets expect lower rates ahead, bond prices rise and yields fall — a standard relief reaction.

But the next day, yields moved higher as investors reassessed the vote and the Fed’s guidance. The split made it clear that future cuts are uncertain and contested, not automatic. Combined with Powell’s emphasis on waiting, tariffs still feeding inflation, and the restart of Treasury bill purchases, bond investors grew less confident that inflation risks are fully behind us.

In simple terms, yields rose because the bond market stopped pricing in a smooth easing path and started pricing in policy uncertainty — the defining feature of what is described as a hawkish cut.

Why that matters for stocks: higher yields raise the cost of borrowing for companies and households, which directly pressures businesses that rely on cheap financing or future growth assumptions. Stocks most exposed tend to fall into three groups:

- Rate-sensitive financials and lenders — regional banks and consumer-credit firms see funding costs rise faster than loan growth, compressing margins.

- Unprofitable or high-multiple tech — many AI, software, and speculative growth names are valued on profits far in the future; higher yields reduce the present value of those earnings, pushing valuations lower.

- Highly leveraged companies — firms funding expansion with debt face higher interest expense just as growth expectations become less certain.

That’s why the post-cut rise in yields mattered: even with rate relief, financial conditions are not easing cleanly, and the stocks that rallied hardest on hopes of an easy Fed path remain the most vulnerable if yields keep pushing higher.

In addition to yields moving higher, signs of that pressure are now emerging in AI infrastructure itself.

Oracle Signals a Pause in AI Infrastructure Timelines

AI infrastructure has been doing the heavy lifting for U.S. growth. Data-center spending — especially tied to AI — accounted for roughly 92% of total U.S. GDP growth in early 2025, making it one of the few areas still driving incremental investment as financial conditions tightened elsewhere.

That’s why Oracle’s update matters. The company disclosed that some of the large data centers it is building for OpenAI have been pushed back to 2028 from 2027, citing labor and material constraints. While Oracle emphasized that its contractual commitments remain intact, the timing shift is meaningful. These projects were expected to support near-term capital spending, construction activity, and demand across chips, power equipment, networking, and industrial supply chains.

Oracle is not alone. CoreWeave has also delayed portions of its buildout, and across the AI infrastructure ecosystem, timelines are stretching as financing costs rise and execution risks increase. Even modest delays can have outsized macro effects when they impact the largest source of private investment in the current cycle.

When AI Capex Slows, the Broader Economy Is Exposed

Outside of data centers, much of the U.S. economy is already under strain. Manufacturing has been contracting for months, housing remains constrained by high mortgage rates, small businesses are freezing hiring, and consumers are pulling back on large purchases. AI capex has helped mask that softness by propping up investment and headline GDP.

If data-center construction slows or slips further into the future, that support fades. Without AI infrastructure contributing in real time, the economy risks revealing the contraction many households and businesses are already feeling — rather than the resilience suggested by aggregate data.

In that sense, Oracle’s delay is not just a company update — it’s a macro warning.

Who Gets Hit First if AI Capex Slows

- Power, cooling, and electrical infrastructure suppliers

Vertiv (VRT), Eaton (ETN) — revenues are closely linked to data-center construction schedules. Delays typically push revenue recognition out, weighing on near-term earnings even if long-term demand remains intact. - Data-center rack, enclosure, and hardware integrators

nVent (NVT), Amphenol (APH), CommScope (COMM) — installations depend on site readiness; timeline slippage directly slows shipments and project milestones. - Electrical equipment, switchgear, and grid components

GE Vernova (GEV), Hubbell (HUBB) — transformer and distribution demand softens when large builds pause, despite multi-year backlog visibility. - Construction, engineering, and installation firms

Fluor (FLR), Jacobs Solutions (J), AECOM (ACM) — labor-intensive phases are easiest to defer, leaving these firms exposed when projects stretch. - Optical, networking, and late-cycle deployment hardware

Ciena (CIEN), Lumentum (LITE), Arista Networks (ANET) — equipment is often installed late in the build cycle, making orders vulnerable to completion delays. - Highly leveraged AI-adjacent operators

Core Scientific (CORZ), DigitalBridge (DBRG) — companies funding expansion with debt face rising interest expense just as execution timelines extend.

Last's Weeks Sector Winners & Losers

Sector performance was mixed, with leadership coming from more cyclical and economically sensitive areas. Materials (XLB) led the market with a +2.40% gain, followed closely by Financials (XLF) +2.37% and Industrials (XLI) +1.40%, signaling renewed interest in areas tied to infrastructure, balance-sheet strength, and nominal growth. Consumer Staples (XLP) and Consumer Discretionary (XLY) also finished higher, suggesting selective risk-taking rather than a broad defensive rotation.

On the downside, Information Technology (XLK) was the weakest major sector, falling -1.98%, reflecting pressure from rising yields and growing scrutiny around AI spending timelines. Utilities (XLU) and Energy (XLE) also lagged, while Real Estate (XLRE) slipped modestly as higher rates continued to weigh on yield-sensitive assets. Communication Services (XLC) finished lower as well, giving back recent gains amid broader tech weakness.

Upcoming Events This Week

Markets face a data-heavy week as focus shifts from Fed policy to delayed but pivotal economic releases. The spotlight is on nonfarm payrolls for October and November and the November unemployment rate, expected to hold at 4.4%. Consensus calls for just 35K job gains in November, reinforcing signs of cooling labor demand.

Inflation remains a constraint. November CPI is expected at 3.2% headline and core, still well above the Fed’s target, while October retail sales are forecast to rise only 0.2%, signaling a softening consumer.

Additional reads — December flash PMIs, regional manufacturing surveys, housing sentiment, and existing home sales — will help markets reassess growth after weeks of trading on incomplete data due to the shutdown.

Earnings from Micron, Accenture, FedEx, and Nike will offer real-time checks on enterprise spending, trade flows, and consumer demand.

Company News

LevelFields AI Stock Alerts Last Week

RIVN +12% After Entering Quick Sprints Scenario on AI & Autonomy Push

Rivian (RIVN) surged 12% in a single session after being included in our Quick Sprints scenario, following the company’s first Autonomy & AI Day, where it unveiled a major push into AI-driven vehicles and autonomy.

Rivian announced it has developed custom AI chips, a proprietary autonomy computer, lidar-enabled sensor stacks, and in-house AI models to power advanced self-driving features in its next-generation vehicles. The company also introduced Autonomy+, a subscription-based driver-assistance platform launching in early 2026, priced at $2,500 upfront or $49.99 per month — undercutting Tesla’s FSD pricing.

Management framed the strategy as a shift toward an “AI-defined vehicle,” opening the door not just to hands-free driving across millions of U.S. road miles, but eventually robotaxi and rideshare opportunities. While Rivian remains under pressure amid slowing EV demand, the announcement reignited momentum by refocusing investor attention on long-term software, AI, and platform optionality, rather than near-term vehicle sales alone.

ASYS +19% on Buyback Authorization

Amtech Systems (ASYS) jumped 19% in one day after announcing that its board authorized a $5 million share repurchase program, allowing the company to buy back stock through open-market purchases, private transactions, block trades, or Rule 10b5-1 plans.

The buyback represents a meaningful capital allocation signal relative to ASYS’s size, tightening share supply and reinforcing management’s confidence in the company’s valuation and outlook. The move immediately boosted sentiment and positioned ASYS as a high-momentum name into year-end.

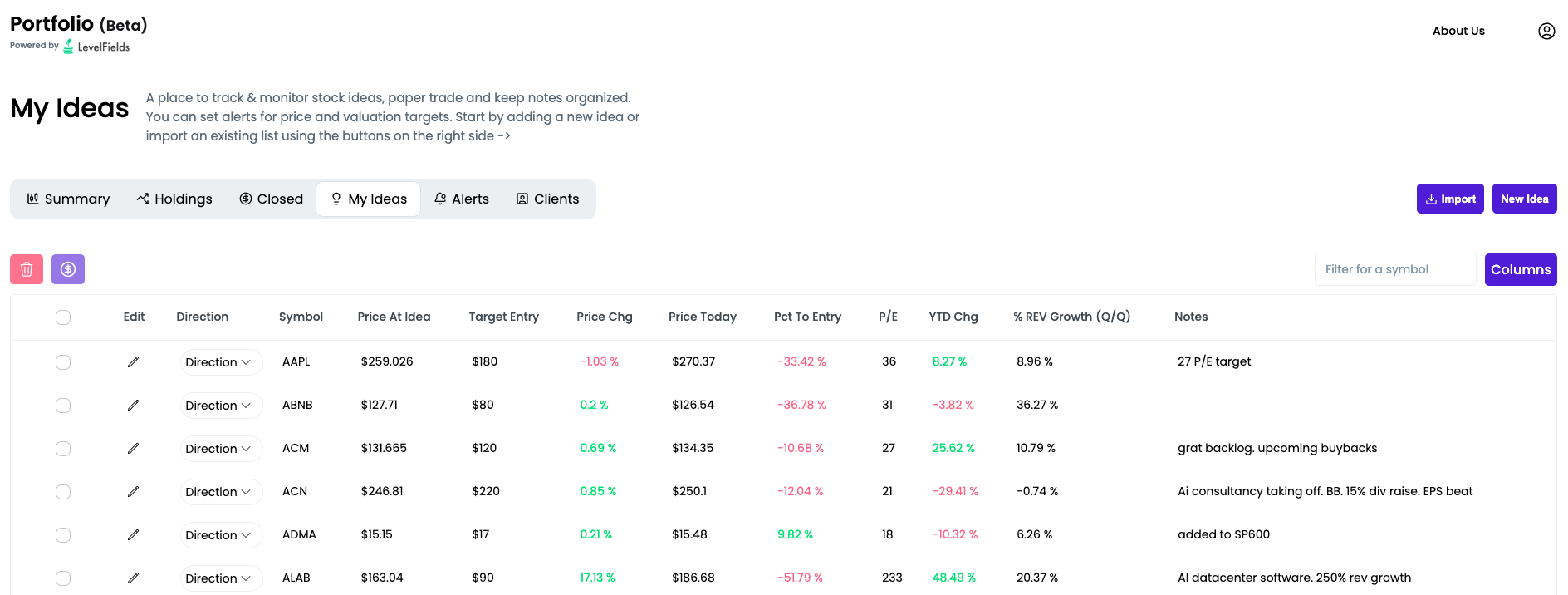

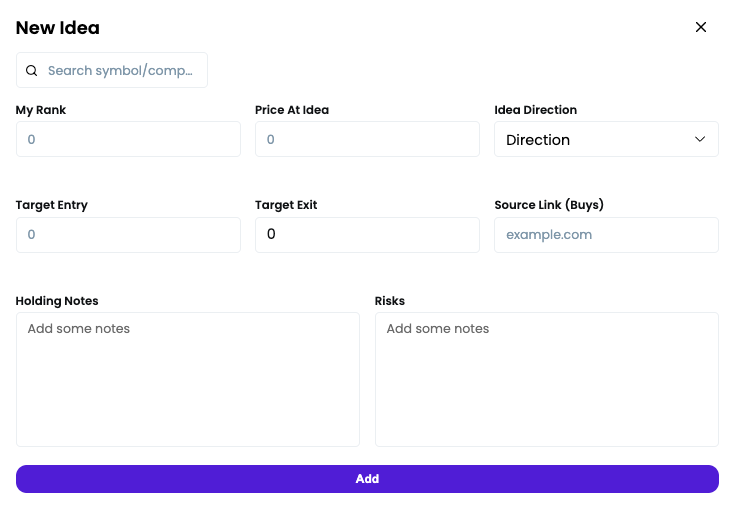

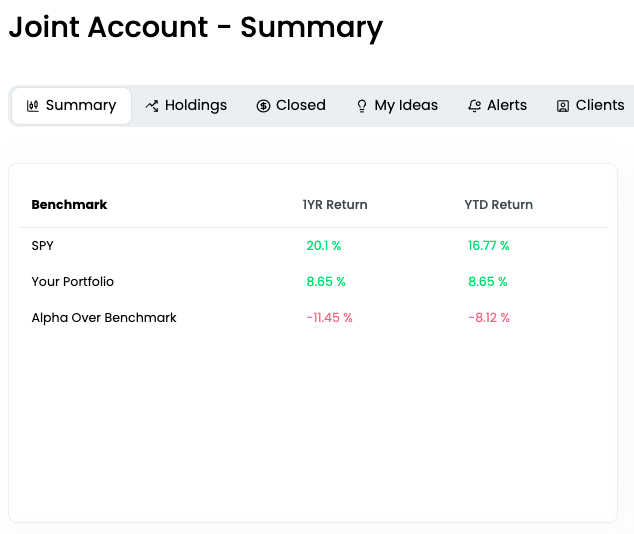

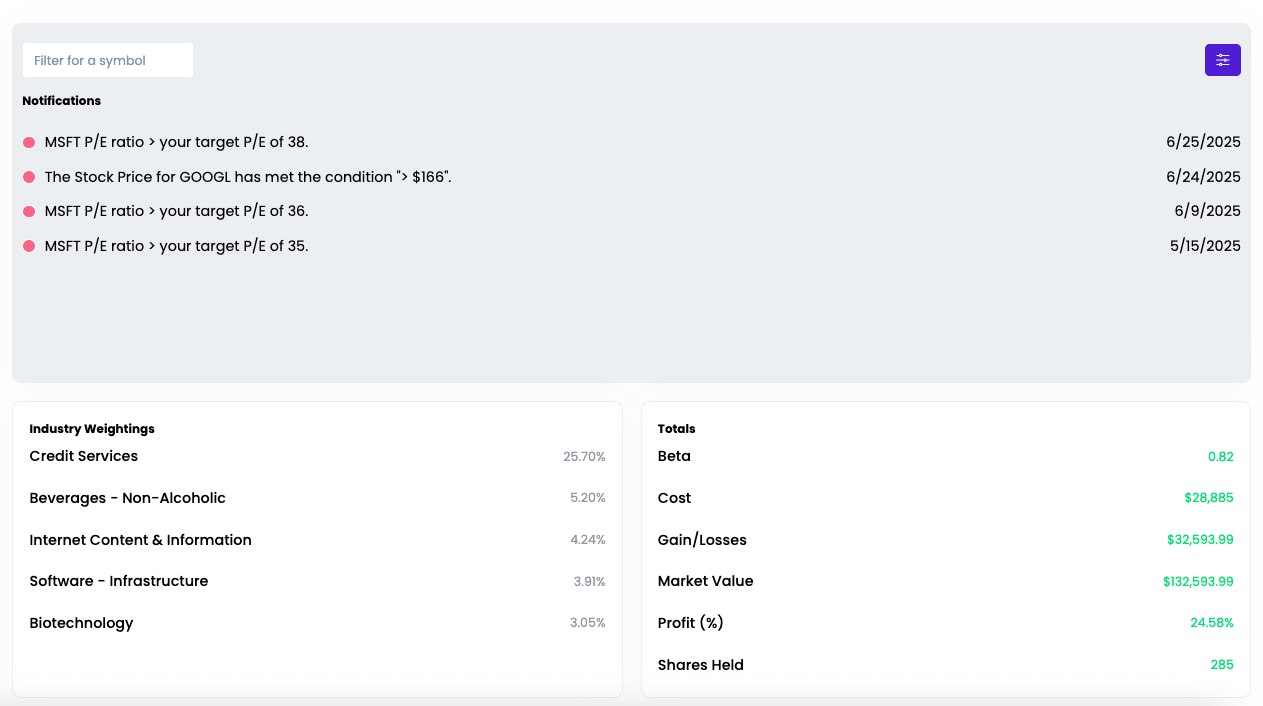

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.org