.png)

L1 Weekly Stock Market News Analysis

January 11th, 2025

TLDR:

Markets enter the new week against a backdrop of escalating geopolitical signals as Venezuela, Iran, and Greenland converged into a broader narrative around energy security, strategic control, and U.S. assertiveness. The aftermath of the U.S. operation in Venezuela, renewed pressure on Iran amid expanding protests, and intensified rhetoric around U.S. control of Greenland have collectively refocused attention on oil, shipping routes, critical materials, and global power dynamics. With desks fully reopened after the holiday slowdown, investors are now assessing how these developments could reshape energy flows and geopolitical risk premia.

Equity markets reflected a risk-on rotation, led by Consumer Discretionary (XLY +5.12%), Materials (XLB +4.64%), and Industrials (XLI +2.50%), signaling renewed appetite for cyclical and resource-linked exposure. Energy (XLE +2.23%) also advanced as geopolitical developments reinforced the strategic value of secure supply. Most defensive sectors participated modestly, while Utilities (XLU -1.55%) lagged, underscoring sensitivity to rates rather than risk aversion.

Looking ahead, attention shifts to a data-heavy global week that will help reset expectations early in 2026. In the U.S., inflation, retail sales, producer prices, housing data, and the start of major bank earnings will shape views on growth and Fed policy amid internal divisions.

Venezuela, Greenland, and Iran Converge

This week, three separate developments highlighted a more assertive U.S. posture toward strategic control, energy security, and geopolitical risk.

In Venezuela, the U.S. continues to consolidate the aftermath of its early-January operation that removed President Nicolás Maduro. Naval enforcement and tanker interdictions in the Caribbean have followed, signaling tighter U.S. oversight of energy flows and shipping routes in the Western Hemisphere.

In Iran, protests have intensified and spread across major cities, raising the possibility of deeper political instability. President Donald Trump has publicly warned that the U.S. could strike Iranian targets if the regime escalates violence against protesters, and U.S. officials have confirmed that military options are under review — developments markets are watching closely given Iran’s role in global energy supply and regional stability.

At the same time, Trump escalated rhetoric around Greenland, renewing his long-standing push to bring the island under U.S. control to counter perceived Russian and Chinese influence. Administration officials have discussed a range of options — from lump-sum payments to residents to encourage secession from Denmark, to the use of the U.S. military as an option for acquiring the territory — though Denmark and Greenlandic leaders have firmly rejected any change in sovereignty.

Viewed together, these developments point to a common theme: energy, materials, and strategic location are increasingly being treated as security issues, not just diplomatic ones.

Why Greenland Matters — Geography, Materials, and Water

Greenland’s importance rests on three pillars: location, materials, and water.

Geography.

Greenland sits between North America and the Arctic, placing it at the center of missile-warning systems, space surveillance, and monitoring of North Atlantic and emerging Arctic shipping routes. As ice continues to retreat, both commercial and military traffic through the Arctic are expected to increase. The U.S. already operates from Pituffik Space Base, which plays a key role in early warning and space monitoring.

Materials.

Greenland holds deposits of rare earth elements, uranium, and iron ore, all of which align with current U.S. supply-chain vulnerabilities:

- Rare earths are critical for magnets used in EVs, wind turbines, semiconductors, radar systems, and missile guidance. China dominates global processing.

- Uranium supports nuclear power and fuel cycles, which are increasingly viewed as essential for grid reliability as electricity demand rises from AI and data-center expansion.

- Iron ore underpins steel production, which remains foundational for defense manufacturing, shipbuilding, infrastructure, and energy projects.

In an environment where export controls and trade restrictions can disrupt supply chains quickly, access to these materials has shifted from a cost issue to a national-security concern.

Water — an emerging AI constraint.

Greenland also contains one of the world’s largest freshwater reserves, stored in its ice sheet. As AI infrastructure scales, water availability is becoming a more visible constraint.

Modern data centers require large amounts of freshwater for cooling. When accounting for on-site cooling and the water used by power plants supplying electricity, each AI query indirectly consumes an estimated 1–3 bottles of freshwater. As AI workloads grow, water is increasingly treated as a limiting input alongside power and land.

This is already driving long-term capital spending on water treatment, cooling systems, and metering infrastructure, reflecting expectations that AI growth will materially increase water demand over time.

The National Security Agenda Behind It

These actions align closely with the National Security Strategy of the United States of America, released by the White House in November 2025.

At a high level, the strategy makes a clear shift away from managing a fully globalized system toward prioritizing control, resilience, and regional dominance where it matters most.

The strategy emphasizes four main objectives:

- Reduce reliance on adversaries for energy, critical minerals, technology inputs, and industrial capacity.

- Secure access to essential materials and infrastructure, either domestically or through tightly aligned partners.

- Protect key geography and chokepoints — shipping lanes, airspace, energy routes, and strategic territory.

- Use economic power alongside military force, including tariffs, sanctions, export controls, investment, and direct participation in strategic industries.

A defining feature of current U.S. policy is an expanded Strategic Reserve approach — not limited to stockpiling materials, but increasingly expressed through equity stakes, project financing, and long-term offtake agreements across critical supply chains. While not named explicitly in the National Security Strategy, this approach aligns with its emphasis on supply-chain security and resilience.

In practice, this has already included U.S. government stakes or direct backing in companies such as Intel (INTC) (advanced semiconductors), MP Materials (MP) (rare earths), United States Antimony (UAMY) (strategic metals), Lithium Americas (LAC) (battery materials), and Trilogy Metals (TMQ) (copper and zinc). The objective is to ensure continuity of supply during geopolitical stress rather than relying on global markets alone.

How the strategy breaks the world down

Western Hemisphere (highest priority).

The strategy treats the Americas as the core security zone. Preventing hostile powers from controlling energy resources, shipping routes, or governments in the region is a top objective. Venezuela fits squarely here: energy reserves, proximity to U.S. trade routes, and foreign influence made it a direct concern.

Asia-Pacific (systemic competition).

China is framed as the primary long-term competitor, particularly in technology, manufacturing, and critical minerals. Export controls, tariffs, and reshoring efforts are aimed at reducing exposure to Chinese leverage — especially in rare earths, semiconductors, and advanced manufacturing.

Middle East (stability and energy security).

The strategy emphasizes preventing nuclear proliferation, protecting energy markets, and avoiding regional wars that could disrupt global supply. Iran is central to this framework due to its nuclear program, missile capabilities, and role in oil markets.

Arctic (emerging theater).

The Arctic is treated as an emerging strategic zone due to shipping routes, early-warning systems, and untapped resources. Greenland’s location and materials place it directly within this category.

Venezuela, Iran, and Cuba in the Context of U.S. Strategy

Venezuela aligns with the strategy’s explicit Western Hemisphere priority. The National Security Strategy emphasizes preventing rival powers from gaining durable influence in the Americas, protecting nearby energy supply chains, and using limited, decisive actions to restore U.S. leverage rather than prolonged intervention. Venezuela’s location, oil infrastructure, and growing ties with China and Russia placed it squarely within that scope. The U.S. approach — leadership removal paired with maritime enforcement and sanctions control — reflects the strategy’s preference for contained operations that reassert control over strategic assets and shipping routes, not nation-building.

Iran fits the strategy’s Middle East posture, which prioritizes deterrence, energy stability, and non-proliferation, while avoiding large-scale occupation. The document does not call for regime change as a standing objective, but it does frame internal instability in adversarial states as a risk that must be managed to prevent nuclear escalation, regional conflict, or disruption of global energy flows. U.S. signaling around Iran — emphasizing consequences for violent repression and nuclear expansion — is consistent with a strategy focused on pressure, signaling, and containment, rather than direct governance of outcomes.

At the same time, Cuba is emerging as a consequential secondary pressure point in the hemisphere. Following the U.S. capture of Nicolás Maduro and a strict oil blockade, President Donald Trump declared that no more Venezuelan oil or money will go to Cuba, urging Havana to strike a deal with Washington and underscoring the island’s deep reliance on Venezuelan fuel. Cuban leaders have rejected these overtures, emphasizing sovereignty and signaling resistance, but the cutoff of subsidized Venezuelan crude is expected to intensify economic hardship on the island. This escalation reflects the same hemispheric strategic logic: by severing Cuba’s energy lifeline, the U.S. increases pressure on a key ally of Venezuela and tests the resilience of regional allies against adversarial influence. It also dovetails with longstanding U.S. policy frameworks aimed at limiting external support to regimes viewed as unfriendly — reinforcing that energy leverage and geopolitical positioning in the Americas remain central to strategic objectives.

Taken together, these cases reflect a common pattern outlined in the strategy:

- Geographic prioritization (Americas first, then critical theaters),

- Targeted force or pressure instead of open-ended war, and

- Leverage over outcomes (energy access, shipping security, deterrence credibility) rather than ideological transformation.

How to Position

Greenland / Arctic / Critical Minerals

- Critical Metals Corp. (CRML) — Controls the Tanbreez rare-earth project in Greenland, positioning it to benefit from U.S. and allied efforts to secure non-China sources of rare earths for defense, EV, and clean-energy supply chains.

- MP Materials (MP) — Transitioning from mining into integrated rare-earth processing and magnet production, benefiting from policy and Pentagon support aimed at reducing dependence on Chinese supply.

- Energy Fuels (UUUU) — A major U.S. uranium producer that has expanded into rare-earth oxides, aligning with efforts to secure domestic nuclear fuel and strategic mineral supply chains critical to energy and defense.

- Trilogy Metals (TMQ) — Developing copper and zinc projects in Alaska with U.S. backing; copper is a strategic input for electrification, grid reliability, and defense manufacturing.

Venezuela / Hemispheric Energy Security

- Chevron (CVX) — The only U.S. oil major operating under license in Venezuela, positioned to benefit if sanctions ease and Venezuelan heavy-crude exports resume to U.S. Gulf Coast refineries.

- Valero Energy (VLO) — Gulf Coast refiner configured for heavy sour crude, benefiting from increased nearby supply if Venezuelan exports normalize.

- Marathon Petroleum (MPC) — With extensive Gulf Coast capacity, renewed Venezuelan crude flows could improve utilization rates and refining margins.

Iran Risk / Defense & Deterrence

- Lockheed Martin (LMT) — Leading supplier of missiles, radar, and air-defense systems, benefiting from heightened deterrence and allied defense readiness.

- Northrop Grumman (NOC) — Provider of strategic systems and intelligence capabilities essential for surveillance and deterrence in contested regions.

- Huntington Ingalls Industries (HII) — Builder of naval vessels and surface combatants, supported by increased maritime readiness and enforcement priorities.

- General Dynamics (GD) — Supplier of submarines, armored vehicles, and C4ISR systems, benefiting from defense budgets tied to regional risk and great-power competition.

Last's Weeks Sector Winners & Losers

Sector performance skewed decisively risk-on, with broad-based gains across most major groups. Consumer Discretionary (XLY) led the market higher, rising +5.12%, signaling renewed appetite for cyclical and consumer-facing exposure. Materials (XLB) followed with a +4.64% gain, supported by continued strength in commodities and critical-minerals themes, while Industrials (XLI) advanced +2.50%, reflecting optimism around infrastructure, defense, and manufacturing activity.

Energy (XLE) gained +2.23%, supported by geopolitical developments and tighter control over Western Hemisphere energy flows. Defensive sectors also participated: Consumer Staples (XLP) rose +2.01%, Health Care (XLV) added +1.16%, and Financials (XLF) increased +1.46%. Information Technology (XLK) posted a more modest +1.28%, indicating selective participation amid ongoing scrutiny of AI and capex trends.

The lone laggard was Utilities (XLU), which declined -1.55%, reflecting sensitivity to rate expectations and capital intensity. Real Estate (XLRE) was largely flat, up just +0.30%, as higher financing costs continued to cap upside. Overall, the session reflected a broad rotation toward cyclicals and strategic sectors tied to growth, infrastructure, and resource security.

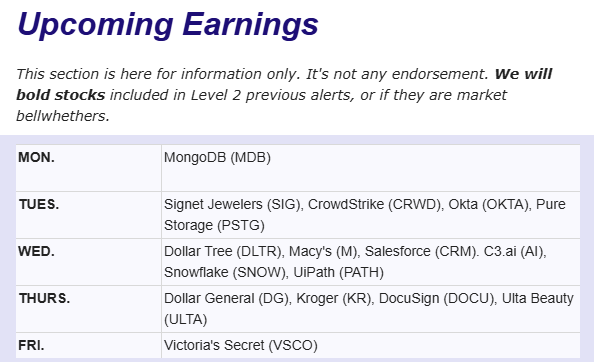

Upcoming Events This Week

The coming week brings key global macro catalysts and the start of U.S. bank earnings. In the U.S., markets will focus on inflation, alongside retail sales, PPI, housing data, and trade figures, as policymakers remain divided over persistent price pressures. Europe will release GDP updates from Germany and the U.K., plus Eurozone production and trade data, while China’s trade and credit figures will shed light on protectionism and manufacturing conditions. Japan’s current account and machinery orders, a Bank of Korea rate decision, and inflation prints from India and Russia round out an event-heavy global calendar.

Company News

LevelFields AI Stock Alerts Last Week

ALT +16.5% on FDA Breakthrough Therapy Designation

Altimmune (ALT) jumped 16.5% after the FDA granted Breakthrough Therapy Designation to pemvidutide for the treatment of MASH (metabolic dysfunction–associated steatohepatitis). The designation followed strong clinical data and signals the FDA’s view that pemvidutide may offer meaningful improvement over existing treatment options. With MASH representing a large, underserved market and heightened regulatory momentum around obesity-linked liver disease, the announcement materially improved visibility into pemvidutide’s development and commercial potential.

Trump Floats 10% Credit Card Rate Cap

President Trump called for a one-year cap on credit card interest rates at 10%, saying Americans have been “ripped off” by high borrowing costs. The outline lacks implementation details and would require Congress to act, leaving its practical path and timing uncertain.

Who this impacts:

- Large U.S. banks / credit card issuers — Higher-rate lending contributes materially to net interest income:

- JPMorgan Chase (JPM)

- Bank of America (BAC)

- Capital One Financial (COF)

- American Express (AXP)

- Citigroup (C)

Capping interest income on credit cards could compress revenues and margins if adopted in law.

- Regional banks / community lenders — Often have a higher share of unsecured lending and could see funding and credit-risk dynamics shift.

- Non-bank lenders & alternative financing — A strict cap could push risk and demand toward unregulated or lightly regulated lenders (e.g., payday lenders, “buy-now-pay-later” firms), which do not fall under traditional rate caps.

Market signal vs. mechanics

The proposal has political traction because lawmakers from both parties have expressed concern over rising consumer borrowing costs. Banking advocacy groups warn a hard cap could reduce credit availability and push borrowers into higher-cost channels.

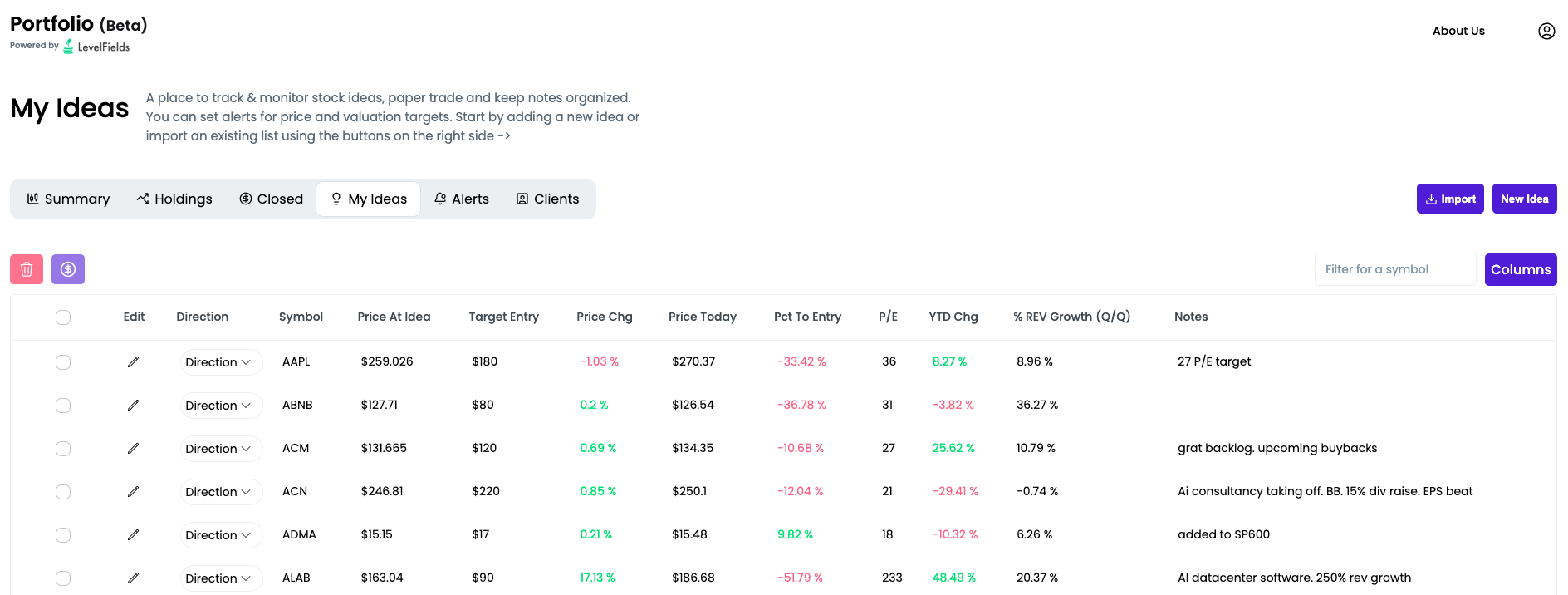

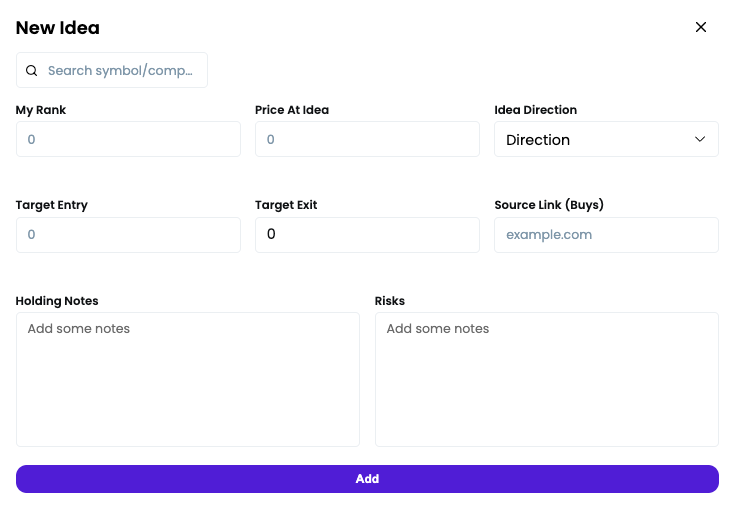

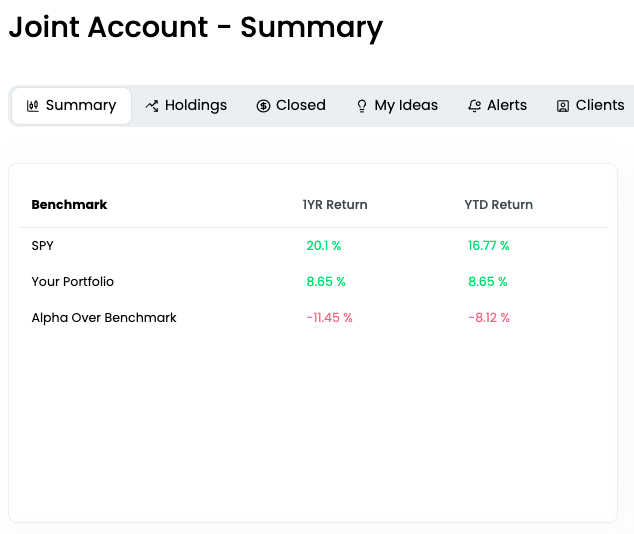

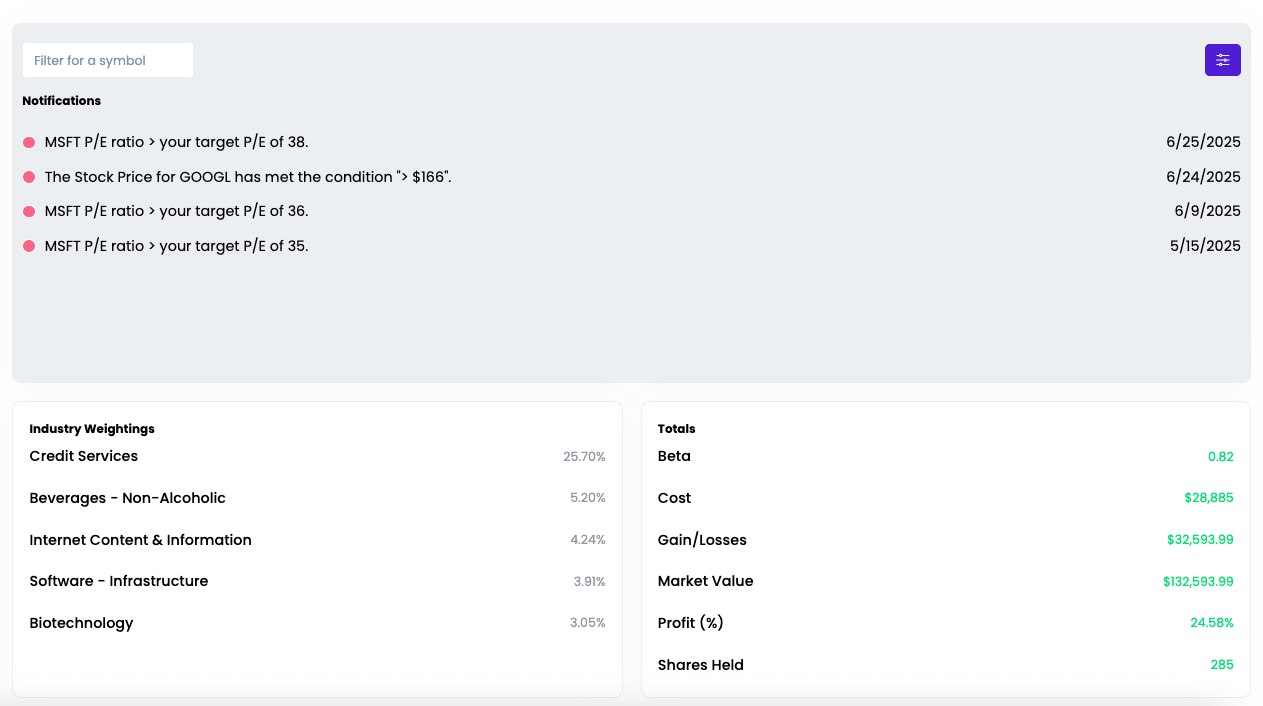

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.org