.png)

L1 Weekly Stock Market News Analysis

January 18th, 2025

TLDR:

Markets enter the new week with tariffs and earnings — not macro data — driving positioning, as developments tied to Greenland, Iran, and recent bank results reshape near-term risk assessment.

On trade, tariffs are increasingly being used as geopolitical leverage rather than traditional trade tools. President Trump’s threat to impose 10–25% tariffs on European countries opposing U.S. pressure over Greenland has put the mid-2025 EU–U.S. trade framework at risk, reopening uncertainty around tariff ceilings, zero-tariff carve-outs, and regulatory cooperation. Separately, the administration’s move to impose a 25% tariff on any country doing business with Iran has raised tensions with China, which remains Iran’s most significant oil buyer. The Iran tariffs land at a sensitive moment, coming just months after the November 2025 U.S.–China trade deal, which depended on China suspending rare-earth export controls, rolling back retaliatory tariffs, and reopening agricultural imports while the U.S. paused additional Section 301 actions. Together, these moves underscore growing instability in U.S.–EU and U.S.–China trade relations, particularly around energy, critical minerals, and agriculture.

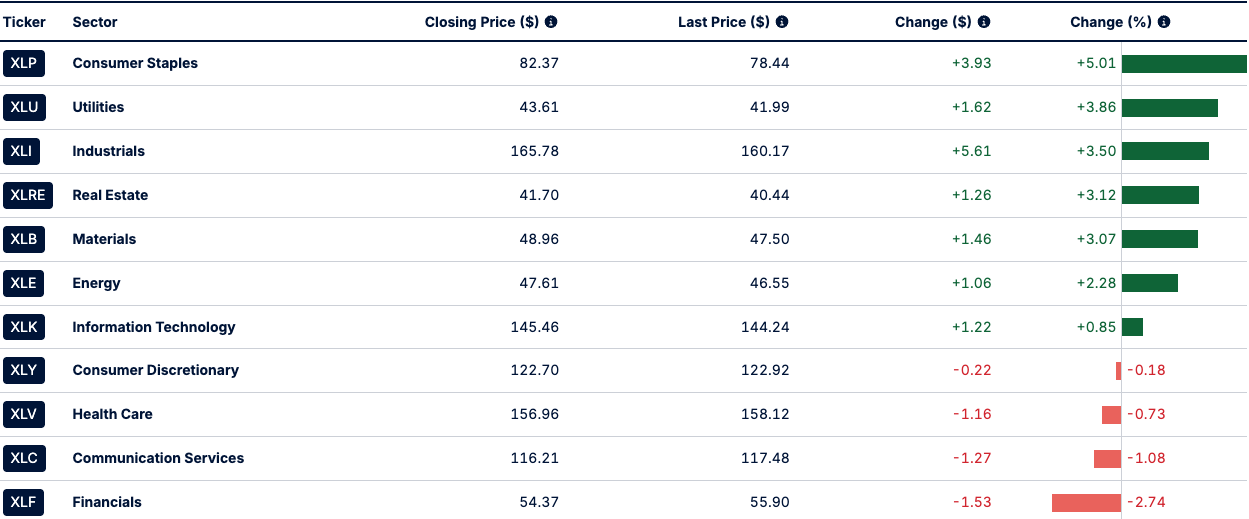

Equity markets reflected a risk-on but selective rotation. Consumer Discretionary (XLY +5.12%), Materials (XLB +4.64%), and Industrials (XLI +2.50%) led gains, signaling renewed appetite for cyclical and domestically anchored exposure. Energy (XLE +2.23%) advanced as tariff and sanction dynamics reinforced the strategic value of U.S.-aligned supply. Information Technology (XLK +1.28%) participated modestly, while Utilities (XLU −1.55%) lagged on rate sensitivity.

Financials underperformed following a round of disappointing bank earnings, with several major lenders missing expectations due to weaker mortgage activity, delayed deal flow, elevated expenses, and uncertainty around a proposed cap on credit-card interest rates. The sector’s weakness reflected earnings pressure rather than systemic stress, with capital-markets-oriented banks holding up better than consumer-exposed lenders.

Greenland Tariffs and the EU’s Trade Deal Threat

Over the weekend, tensions between the United States and Europe escalated sharply after President Trump moved from rhetoric to action, announcing new tariffs on eight European countries opposing Washington’s push to acquire Greenland. Under the plan, a 10% tariff on all goods from Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland will take effect February 1, rising to 25% on June 1, and remain in place until a deal is reached for the purchase of Greenland. All eight countries are NATO members.

European officials responded by warning that the European Union could suspend or halt implementation of the EU–U.S. trade deal agreed in mid-2025, characterizing the tariffs as political coercion rather than trade enforcement. Members of the European Parliament and several national governments said the measures undermine the foundations of the transatlantic relationship and risk triggering a retaliatory spiral.

The EU–U.S. agreement intended to provide predictability for companies operating across the Atlantic. It capped U.S. tariffs on most EU exports at 15%, eliminated tariff stacking, and established zero or near-zero tariff regimes for specific categories such as aircraft and parts, generic pharmaceuticals, chemical precursors, and select natural resources. The framework also included cooperation on metals, supply-chain security, regulatory alignment, and energy trade — including European commitments to procure U.S. LNG, oil, and nuclear energy products.

European leaders have now made clear that this framework itself is in jeopardy. Several officials warned that tying tariffs explicitly to territorial or political concessions crosses a line and may justify suspending the deal’s benefits unless the tariff threats are withdrawn.

Why the Trade Deal Matters for Markets

The EU–U.S. relationship remains the largest bilateral trade and investment corridor in the world, with roughly €1.6 trillion in annual goods and services trade and more than €4 billion crossing the Atlantic each day. The 2025 agreement provided clearer tariff ceilings and regulatory guardrails for firms with significant transatlantic exposure.

If the deal is paused or unwound, the impact is likely to be sector-specific rather than economy-wide, concentrated in industries that relied most on tariff ceilings, zero-tariff carve-outs, and regulatory cooperation — and amplified by the fact that the tariffs are now explicitly framed as conditional leverage, not conventional trade policy.

Industrials & Aerospace

- Aircraft and aircraft parts were placed under a zero-tariff regime.

- Companies with heavy transatlantic exposure — Boeing (BA), Airbus (EADSY), Rolls-Royce Holdings (RYCEY), and BAE Systems (BAESY) — face renewed tariff and delivery-risk uncertainty if the deal is suspended.

Automotive

- Vehicles were covered by a 15% tariff ceiling with no stacking.

- European automakers with significant U.S. exposure — Volkswagen (VWAGY), BMW (BMWYY), and Mercedes-Benz Group (MBGYY) — would be most sensitive to renewed duties and standards risk.

Pharmaceuticals & Chemicals

- Generic drugs, chemical precursors, and related inputs benefited from low or zero tariffs and regulatory cooperation.

- Cross-border operators such as Pfizer (PFE), Merck KGaA (MKGAY), and BASF (BASFY) could see margin pressure if tariff ceilings or mutual recognition are rolled back.

Energy & LNG

- The deal supported European purchases of U.S. LNG and energy products.

- Exporters like Cheniere Energy (LNG) and integrated producers such as Exxon Mobil (XOM) face policy and headline risk if cooperation deteriorates.

Iran Tariffs and the Risk to U.S.–China Trade

The Greenland tariffs were not the only escalation this week. President Trump also announced a 25% tariff on any country doing business with Iran, effective immediately. Unlike the Greenland measures, which target specific European allies, these are secondary tariffs, aimed at coercing third countries into complying with U.S. pressure on Tehran.

The move directly implicates China, Iran’s largest oil customer. China relies on heavily discounted Iranian crude to supply its independent refiners, support domestic margins, and secure energy outside Western control. As unrest deepens inside Iran, Tehran has become even more dependent on Chinese demand — tightening the strategic link between the two.

Crucially, this pressure on Iran comes after China’s oil trade with Venezuela has already been disrupted. China is Venezuela’s largest oil buyer, with Venezuelan crude accounting for roughly 5% of China’s annual oil imports. Following the U.S. operation in Venezuela, Beijing strongly condemned the action — not just for political reasons, but because it exposed China’s vulnerability when sanctioned energy suppliers fall under U.S. influence.

President Trump has indicated that Venezuelan oil will continue flowing to China, but under U.S.-aligned oversight. That distinction matters. Rather than cutting China off, Washington appears to be positioning itself as the intermediary, shaping access, pricing, and investment terms. The practical result is increased U.S. energy leverage, even as China remains formally supplied.

Against that backdrop, the Iran tariffs raise the stakes. By threatening a blanket 25% duty on countries trading with Iran, Washington risks forcing Beijing into a direct trade-off between energy security and access to the U.S. market — just months after the two sides reached a fragile trade deal in November 2025. That agreement rested on China suspending rare-earth and critical-mineral export controls, rolling back retaliatory tariffs, and reopening agricultural imports, while the U.S. paused additional Section 301 actions — the trade-law authority that allows Washington to impose punitive tariffs and restrictions in response to unfair foreign trade practices such as subsidies, forced technology transfer, or market access barriers.

Likely Positively Impacted

Energy leverage / U.S.-aligned supply

- Exxon Mobil (XOM), Chevron (CVX), Cheniere Energy (LNG), Valero Energy (VLO)

U.S. gains pricing and routing leverage as Chinese access to Iranian and Venezuelan crude becomes conditional.

Strategic minerals / reshoring

- MP Materials (MP)

Benefits from reduced tolerance for China-controlled processing.

Likely Negatively Impacted

Technology supply chains (Section 301 & retaliation risk)

- Apple (AAPL), NVIDIA (NVDA), Qualcomm (QCOM), Intel (INTC), Broadcom (AVGO)

Exposure via China manufacturing, end demand, export controls, and non-tariff retaliation.

Agriculture (historical retaliation targets)

- Mosaic (MOS), Archer-Daniels-Midland (ADM)

Industrials & materials with cross-border exposure

- Caterpillar (CAT), Freeport-McMoRan (FCX)

The Supreme Court Decision: Why It Matters

The next major catalyst is the pending decision from the U.S. Supreme Court on whether President Trump can rely on emergency powers to impose broad tariffs. The case is not about whether the President has tariff authority in general, but whether the specific legal justification used in 2025 holds up.

During oral arguments, the Court sent a clear signal. Several justices expressed skepticism that emergency powers can support wide, across-the-board tariffs. At the same time, they explicitly acknowledged that the President retains tariff authority under national-security laws. Justice Kavanaugh stated on the record that if the emergency tariffs are struck down, the President still has Section 232 available, and that the Court was not questioning existing national-security findings. Chief Justice Roberts also pressed the government on what happens to tariffs already collected, signaling serious concern that unlawfully imposed tariffs may not be retained — raising the possibility of very large refunds.

For markets, this creates a sequencing problem rather than a binary outcome.

Using aluminum as a practical example of how this could play out: aluminum tariffs were initially set at 10% under national-security authority in 2018, and later increased substantially in 2025 under emergency powers. If the Court invalidates the emergency justification, tariffs could revert to their prior national-security baseline — even if only briefly — before being re-applied or adjusted under a different authority. That interim gap is where volatility lives.

Stocks exposed to this sequencing include Alcoa (AA) and ATI (ATI). Both could sell off on headlines if protection is perceived to weaken, then rebound once tariffs are reinstated under a national-security framework. This is why the setup is short-then-long in sequence, not a one-directional conviction trade.

The ruling also has important secondary effects. If the Court requires refunds of tariffs collected under an invalid authority, Treasury borrowing would rise, pressuring bond markets and supporting precious metals such as SPDR Gold Shares (GLD) and iShares Silver Trust (SLV).

Beyond metals, the decision would reshape which sectors remain protected. Tariffs tied to national security — metals, critical minerals, and defense-linked inputs — are most likely to persist or return. Consumer goods are not. Retailers such as Costco (COST) and Walmart (WMT), along with apparel and footwear names like Nike (NKE) and Crocs (CROX), would benefit if non-essential tariffs fall and stay lower. Autos remain more exposed, with General Motors (GM) and Ford Motor (F) facing uncertainty if protection weakens.

At the index level, the setup favors higher volatility and domestic exposure. The CBOE Volatility Index (VIX) would likely spike on headlines, while the iShares Russell 2000 ETF (IWM) could outperform due to lower import sensitivity.

Last's Weeks Sector Winners & Losers

Sector performance skewed broadly positive, with leadership from defensive and industrial groups rather than pure cyclicals. Consumer Staples (XLP) led the market, rising +5.01%, reflecting a rotation toward pricing power and earnings stability amid macro and policy uncertainty. Utilities (XLU) also posted strong gains (+3.86%), reinforcing a defensive tilt despite lingering rate sensitivity.

Industrials (XLI) advanced +3.50%, supported by infrastructure, defense, and manufacturing exposure, while Materials (XLB) gained +3.07% on continued strength in commodities and critical-minerals themes. Real Estate (XLRE) added +3.12%, rebounding alongside defensives despite higher-rate headwinds, and Energy (XLE) rose +2.28%, aided by ongoing geopolitical developments and tighter control over Western Hemisphere energy flows.

More growth-oriented sectors lagged. Information Technology (XLK) posted a modest +0.85%, signaling selective participation rather than broad risk-on enthusiasm. Consumer Discretionary (XLY) slipped -0.18%, suggesting consumers remain unevenly positioned amid affordability pressures.

On the downside, Financials (XLF) fell -2.74%, the weakest sector on the day, driven by disappointing earnings from major U.S. banks. Results from large lenders missed expectations, with pressure stemming from weak mortgage activity, elevated expenses, slower deal flow, and uncertainty around potential caps on credit-card interest rates. Health Care (XLV) (-0.73%) and Communication Services (XLC) (-1.08%) also lagged, reflecting stock-specific and earnings-related pressures rather than a broad risk-off move.

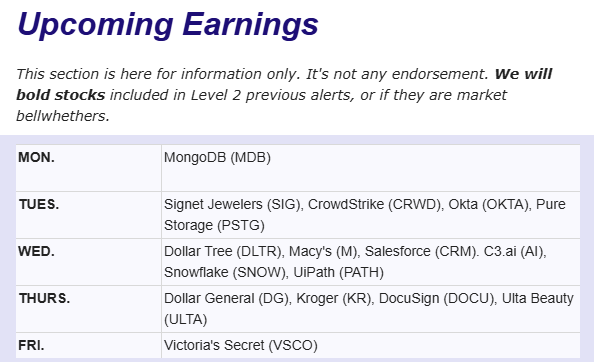

Upcoming Events This Week

U.S. markets are closed Monday for MLK Day, followed by a heavy week of economic data and earnings as agencies catch up after the shutdown. Key macro focus is on personal income and outlays (PCE inflation), another estimate of Q3 GDP (expected to confirm ~4.3% annualized growth), plus PMIs, consumer sentiment (UMich), housing data, and jobless claims.

Globally, investors will watch PMIs across Europe and Asia, UK inflation, jobs, and retail sales, China’s final GDP, and the Bank of Japan policy decision.

Earnings season accelerates with reports from Netflix, 3M, Johnson & Johnson, Visa, Intel, Procter & Gamble, GE Aerospace, Abbott Labs, Charles Schwab, Prologis, Intuitive Surgical, and NextEra Energy.

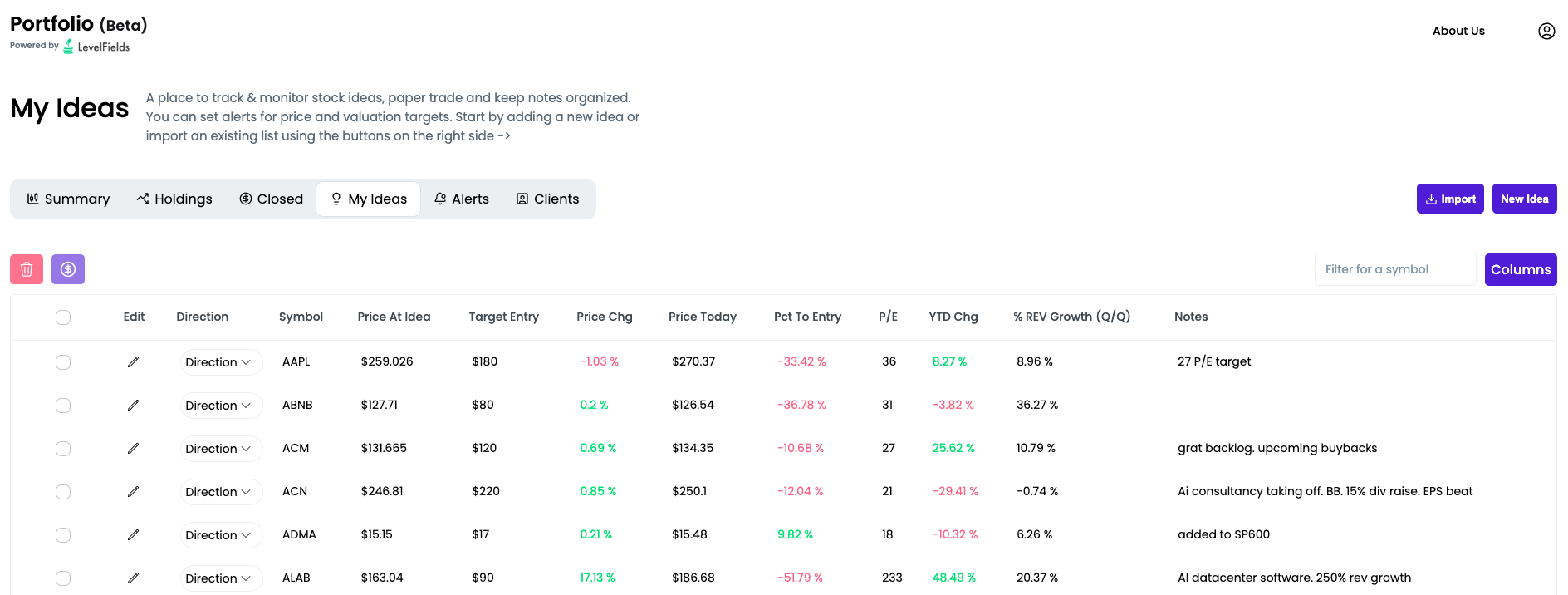

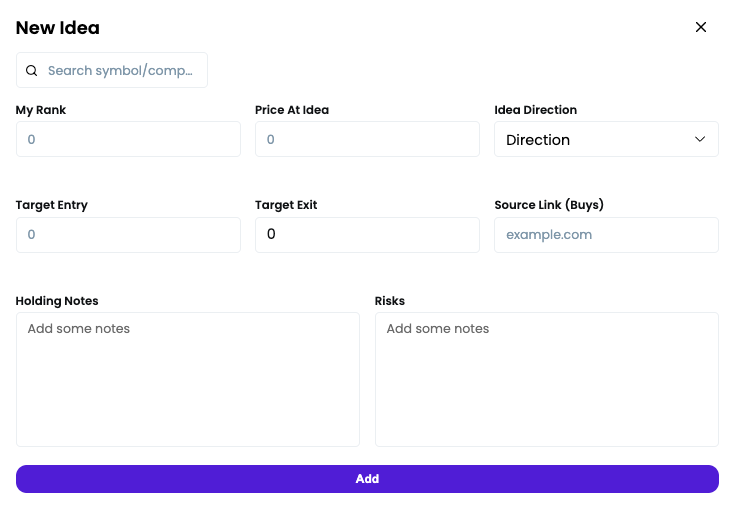

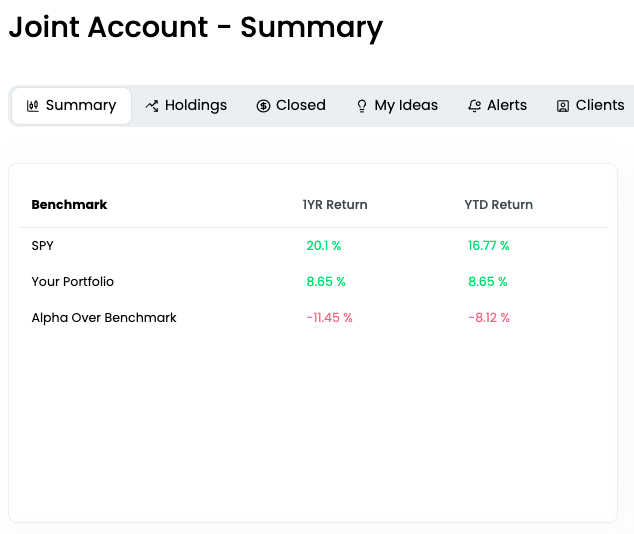

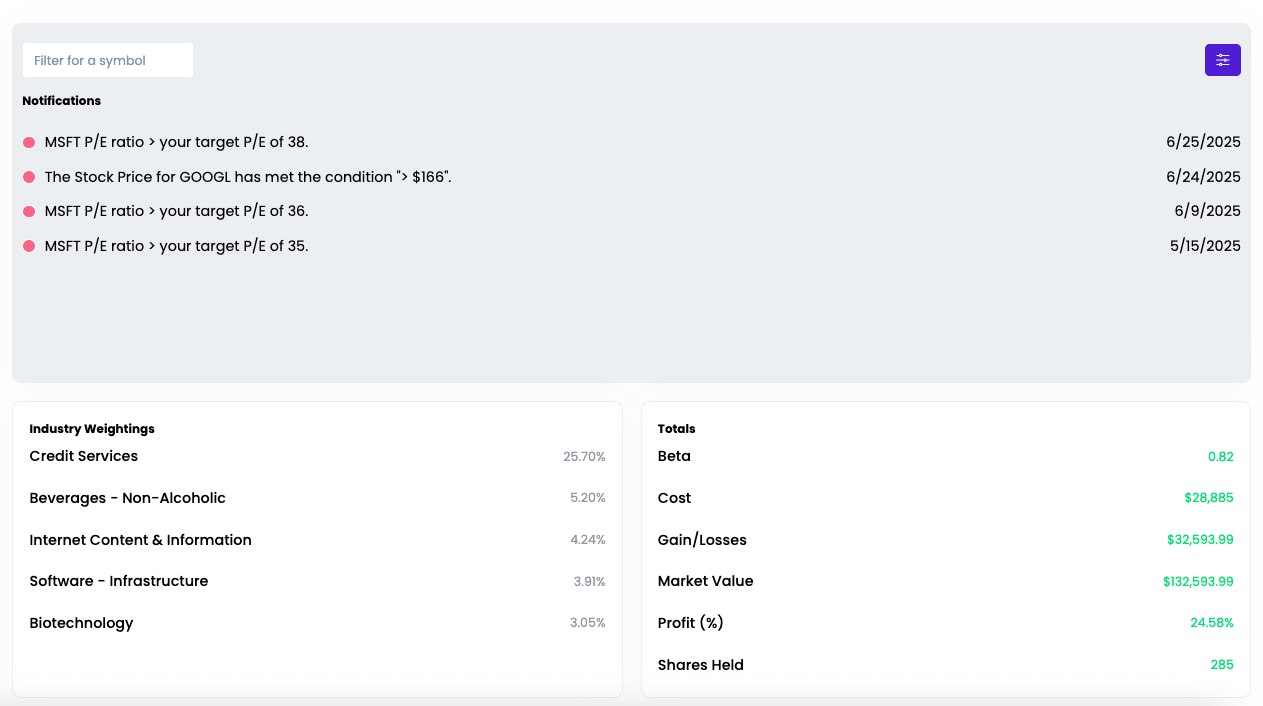

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

Company News

LevelFields AI Stock Alerts Last Week

TryHard Holdings Limited (THH) +138% on $10M Share Repurchase Announcement

TryHard Holdings surged 138% in a single session after announcing a US$10.0 million share repurchase program, equivalent to roughly 25% of its market capitalization. The buyback authorization, funded from existing cash and running through December 2028, signaled strong management confidence in the company’s balance sheet, free cash flow, and long-term growth outlook. Given THH’s small float and microcap profile, the scale of the repurchase dramatically altered supply–demand dynamics, driving an outsized move as investors repriced capital-return optionality.

Bank Earnings: Cracks Beneath the Surface

Big U.S. banks delivered a broadly disappointing earnings round, dragging Financials (XLF) lower despite strong year-over-year stock performance. Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo all missed expectations, citing a mix of higher expenses, weaker mortgage activity, delayed deal flow, and growing uncertainty around a potential credit-card rate cap.

Banks with greater exposure to wealthy clients and capital markets activity — notably Goldman Sachs and Morgan Stanley — held up better, highlighting a widening divergence within the sector. The takeaway for markets: this was not a macro shock, but an earnings quality reset, raising questions about margin durability, regulatory risk, and how much further bank stocks can run without clearer profit momentum.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.org