.png)

L2 Weekly Stock Market News Analysis

February 1st, 2026

TLDR:

Markets head into the first week of February with policy decisions and political uncertainty setting the tone. Last week’s leadership narrowed, and some of the strongest performers earlier this year cooled. Gold, Silver and rare-earth names lagged, reflecting profit-taking after sharp moves, while broader risk appetite remained uneven.

Policy developments took center stage. The Federal Reserve kept rates steady, reinforcing its patient stance, while President Trump formally announced Kevin Warsh as his pick for the next Fed chair, adding a layer of longer-term policy uncertainty without changing near-term expectations. At the same time, Washington failed to reach agreement on funding, and the U.S. government entered a shutdown, increasing headline risk even if immediate economic effects are expected to be limited.

Sector performance reflected caution rather than panic. Energy led the market, supported by geopolitical positioning and energy security themes. Materials posted modest gains, while Health Care edged higher as investors sought relative stability. Most other sectors were flat to lower. Technology and Financials underperformed, while Real Estate and Utilities were the weakest, continuing to feel pressure from rates and funding costs. Overall leadership remained narrow, not indicative of a broad risk-on move.

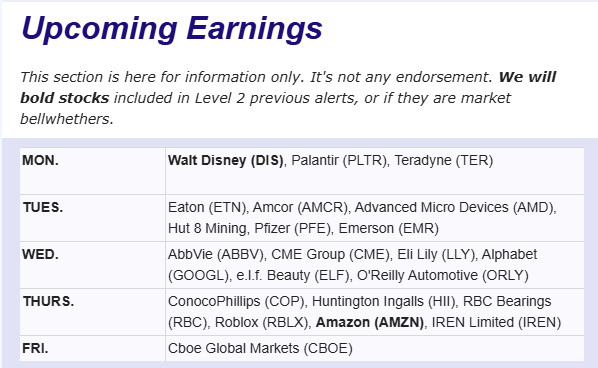

Looking ahead, the week brings a dense calendar of labor market data, including the jobs report, JOLTS, ADP, and Challenger layoffs, alongside ISM manufacturing and services PMIs and University of Michigan consumer sentiment. On the earnings front, results from Amazon, Alphabet, AMD, Palantir, and Qualcomm will shape views on big tech and AI-related spending. Globally, central bank decisions from the ECB, Bank of England, and Reserve Bank of Australia, along with Eurozone inflation and China PMIs, will add to policy and growth signals.

The setup remains one of selectivity and sensitivity to headlines, with markets balancing slowing momentum, policy transitions, and political risk rather than responding to a single dominant macro driver.

The Fed: Rates Hold, and Patience Is the Message

The Fed kept interest rates unchanged this week, holding them in the 3.5%–3.75% range after several cuts last year. That move was widely expected. The more important takeaway was the message behind it: the Fed isn’t rushing into the next cut.

Fed Chair Jerome Powell said rates are now close to a normal level for the economy. Inflation has eased but remains above target, and the job market — while cooling — is still holding together. As a result, the Fed is taking a cautious, meeting-by-meeting approach rather than signaling near-term easing. Markets now see little chance of a March cut, with later in the year looking more plausible if inflation continues to trend lower.

Adding to the backdrop, President Trump has formally nominated Kevin Warsh to succeed Powell when his term ends in May. Markets view Warsh as experienced and credible, not someone likely to force abrupt changes. While Trump has been vocal about wanting lower rates, policy decisions are made by committee, limiting the scope for politically driven swings.

Bottom line: the Fed is signaling patience. Any rate cuts ahead are likely to be gradual and dependent on clear progress in inflation and employment — not on urgency or leadership headlines.

What a Warsh Fed Likely Means in Practice

Despite the attention around the leadership change, the practical reality is that Fed policy is unlikely to shift quickly. Decisions require consensus, and recent votes show internal debate but no clear push toward a new direction.

Warsh’s views fall within the mainstream of central banking. While he has criticized some past policies, his approach doesn’t imply sudden tightening or easing. Where change could emerge over time is in how the Fed approaches its large role in markets. Warsh has argued for a smaller balance sheet and a more limited footprint, but changes of that scale require planning and broad agreement — making them a longer-term issue rather than an immediate catalyst.

Ultimately, the data still dominates. If inflation cools further and hiring weakens, cuts later this year remain possible. If growth stays firm and price pressures persist, the Fed may stay on hold. Leadership sets the tone, but outcomes still depend on the numbers.

Market Implications: Positioning Is the Real Risk

The market reaction to Warsh’s nomination wasn’t about an immediate policy shift — it was about positioning. Coming into February, many trades were built on falling rates, a weaker dollar, and the assumption that the Fed would quickly step in if markets wobbled.

That assumption is now being tested. Even without a policy change, the perception of a less reflexive Fed was enough to trigger reversals. Metals, which had surged on debasement fears and momentum, snapped lower as crowded trades unwound. Emerging markets and other dollar-sensitive assets also look more vulnerable if U.S. rates stop drifting down or the dollar stabilizes.

Equities held up better, but the tone shifted. Stocks softened as longer-term yields moved higher, suggesting investors are reassessing how much policy and liquidity support they can count on rather than pricing in an outright downturn. The pressure is most visible in areas that rely heavily on cheap financing, long-duration cash flows, or continuous access to capital.

Most exposed areas include:

• High-multiple growth and software — companies like Snowflake, Palantir, and ServiceNow, where valuations are sensitive to higher long-term rates.

• Rate-sensitive real estate and infrastructure — including Prologis and American Tower, where funding costs matter as much as operating fundamentals.

• Leveraged cyclicals and smaller caps — firms dependent on refinancing or capital markets access, where higher yields quickly tighten financial conditions.

The Dollar: Weakness Without a Breakdown

The dollar has fallen sharply in recent weeks, reviving talk that investors are abandoning U.S. assets. That story, however, is starting to look overdone. Positioning data suggest many traders are already leaning heavily toward a weaker dollar, and history shows that when a trade becomes this crowded, the risk often shifts toward a pause or reversal rather than a straight-line continuation.

Comments from Kevin Hassett addressed one of the market’s biggest concerns: whether dollar weakness is being encouraged by policy. Hassett pushed back on the idea that the administration wants a weaker currency, arguing that recent moves reflect global forces — shifting growth patterns, capital flows, and interest-rate expectations — rather than a deliberate attempt to devalue the dollar.

That distinction matters. When the dollar softens because economic conditions are improving elsewhere, the move tends to be gradual and manageable, often supporting global trade and corporate earnings. A dollar weakened by policy intent, by contrast, would signal a willingness to tolerate higher inflation and currency instability, which can undermine investor confidence. Hassett’s remarks were meant to reassure markets that recent dollar weakness is incidental, not strategic.

What’s notable is that the dollar’s pullback doesn’t fully align with the U.S. economic data. Near-term indicators remain firm, with real-time tracking models showing strong momentum — the Atlanta Fed’s GDPNow estimate currently points to fourth-quarter growth above 4%, well above long-term trend.

Looking further ahead, the outlook remains constructive. Forecasts for 2026 GDP are clustering closer to 2.5%, higher than many earlier projections, supported by consumer spending, tax policy tailwinds, and productivity gains. Together, those signals argue against a narrative of deteriorating U.S. growth and make aggressive bets against the dollar harder to justify.

That combination reduces the appeal of pressing the short-dollar trade. Currencies typically weaken when growth is rolling over or capital is fleeing. Neither condition is clearly present. Instead, the recent decline increasingly looks driven by positioning and sentiment rather than fundamental weakness.

A weaker dollar also cuts both ways for markets. In the short term, it can weigh on U.S. equities by raising import costs, squeezing margins for companies with global supply chains, and complicating inflation and interest-rate dynamics. It can also act as a signal of uncertainty, encouraging caution rather than risk-taking.

Over the longer term, however, a modest and orderly decline in the dollar can support U.S. competitiveness — and that aligns with the Trump administration’s broader push to expand American exports and rebuild domestic manufacturing. A softer currency makes U.S. goods more price-competitive abroad and boosts the overseas earnings of multinational firms, improving trade balances without relying on explicit subsidies or mandates.

That’s why periods of controlled dollar weakness often coincide with stronger industrial activity, rising exports, and improving manufacturing margins. But this only works when the move is gradual and rooted in economic conditions, not policy shock. When dollar softness reflects growth, investment, and productivity gains rather than forced devaluation, it can reinforce export momentum instead of undermining confidence.

More Likely to Struggle

Import-heavy, consumer-facing companies

- Target (TGT)

- Walmart (WMT)

- Nike (NKE)

Higher import costs squeeze margins as consumers remain price-sensitive.

Transportation and rate-sensitive financials

- Delta Air Lines (DAL)

- PNC Financial Services (PNC)

Rising costs and rate uncertainty weigh on profits.

Potential Beneficiaries

Global exporters and multinationals

- Microsoft (MSFT)

- Apple (AAPL)

- Coca-Cola (KO)

Foreign revenue translates into higher dollar earnings.

Industrials and commodities

- Caterpillar (CAT)

- Freeport-McMoRan (FCX)

U.S. exports become more competitive; commodity prices often get support.

Last's Weeks Sector Winners & Losers

Sector performance was uneven, with strength concentrated in a handful of areas rather than spread across the market. Gains were led by Energy and Communication Services, while Health Care and consumer-focused sectors lagged.

Energy (XLE) was the clear leader, rising +3.27%, as oil-related stocks benefited from ongoing geopolitical concerns and renewed attention on U.S. and regional energy supply. Communication Services (XLC) followed closely, up +3.05%, helped by strength in large-cap media and internet names. Utilities (XLU) gained +1.45%, suggesting some defensive positioning despite recent rate volatility.

Technology (XLK, +1.37%) and Materials (XLB, +0.97%) also moved higher, pointing to selective buying rather than broad enthusiasm. Real Estate (XLRE) and Industrials (XLI) posted modest gains, finishing slightly positive but without strong momentum.

On the downside, Health Care (XLV) was the weakest sector, falling –2.82%, driven by policy and reimbursement uncertainty. Consumer Discretionary (XLY) declined –1.17%, reflecting pressure on spending-sensitive stocks. Financials (XLF) slipped –0.48%, while Consumer Staples (XLP) edged lower (–0.17%), showing limited demand for traditional defensive plays.

Upcoming Events This Week

The first week of February brings heavy macro and earnings risk after a volatile start to the year marked by sharp moves in metals, dollar uncertainty, and Trump’s nomination of Kevin Warsh as Fed chair. In the U.S., markets will focus on the January jobs report, JOLTS, ADP, and Challenger data, alongside ISM PMIs and consumer confidence for clues on growth and labor momentum. Earnings continue with Amazon, Alphabet, AMD, Palantir, and Qualcomm shaping views on AI and big tech. Globally, central banks including the ECB, BoE, and RBA meet, while Eurozone inflation and China’s PMIs add to the policy and growth picture.

Company News

LevelFields AI Stock Alerts Last Week

- Redwire (RDW) +30% — Missile Defense Contract Award

Redwire shares surged 30% in a single session after the company was selected by the Missile Defense Agency for the $151 billion, multi-vendor SHIELD IDIQ program supporting U.S. homeland defense. While awards under the contract will be competed over time, inclusion positions Redwire for potential billion-dollar opportunities, sharply improving long-term revenue visibility and reinforcing its role in defense and space infrastructure. - Liberty Energy (LBRT) +17% — Dividend Increase

Liberty Energy jumped 17% after announcing a 13% increase in its quarterly cash dividend to $0.09 per share, beginning in Q4 2025. The hike signals confidence in cash flow durability and capital discipline, particularly as energy markets stabilize, and improves the stock’s appeal to income-focused investors. - Merchants Bancorp (MBIN) +15% — Share Repurchase Program

Merchants Bancorp rallied 15% after its board approved a $100 million stock repurchase program, running through December 31, 2027. The buyback represents a meaningful return of capital, highlights balance-sheet strength, and supports earnings per share through reduced share count amid a volatile regional banking backdrop. - Tesla — The AI dream keeps the stock afloat, but the core business is still under pressure

Tesla went into earnings with investors increasingly framing it less as a car company and more as a long-dated AI, robotics, and autonomy platform. That narrative mattered because the core automotive business has been under strain for some time — slowing deliveries, heavier discounting, and margin compression as competition intensifies and consumer incentives fade.

The earnings report didn’t reverse that reality. Revenue fell year over year, vehicle deliveries declined, and free cash flow dropped sharply as spending ramped. Even with a modest earnings beat, the underlying picture was clear: selling cars is getting harder, not easier, and near-term profitability is being sacrificed to fund long-term bets.

Where Tesla surprised was in reinforcing the AI optionality investors want to believe in. Energy storage delivered record results, with Megapack deployments accelerating and profits hitting new highs. More importantly for the stock, Tesla disclosed a $2 billion investment in xAI, formally tying its future to Musk’s broader AI ecosystem. That move reframed the quarter — not as an auto slowdown, but as a stepping stone toward robots, robotaxis, and physical AI.

That framing helped the stock rebound after an initial selloff. Investors weren’t buying the earnings; they were buying the strategy. The problem is timing. Robotics, Optimus, and large-scale robotaxi deployment remain expensive, uncertain, and years away from meaningful cash generation, while the automotive business is still what pays the bills today.

Tesla didn’t deliver a clean earnings turnaround. Instead, it leaned harder into the future to offset present-day weakness. As with Intel, the stock isn’t trading on what the company is earning now — it’s trading on whether management can bridge the gap between an increasingly pressured core business and ambitious, capital-intensive bets that haven’t yet proven they can scale profitably.

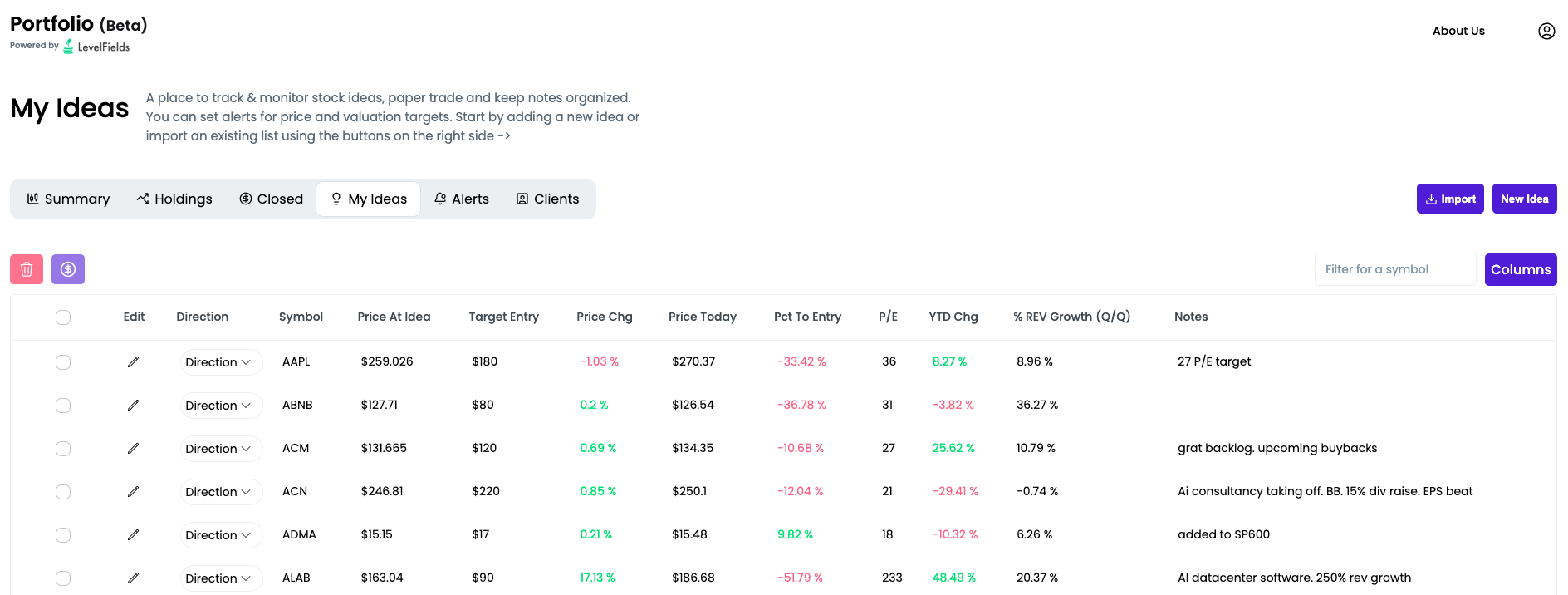

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.org